Are you constantly overshooting your budget?

You could shift the blame to expensive developers, but you’d be missing something.

Your costs are likely snowballing because you underestimated a production-ready financial product that needs:

- Security

- Compliance

- Third-party integrations

- Fraud prevention

- Scalability

By the time those requirements pop up, the original budget will no longer be true to life.

That’s why estimating fintech app development cost is so difficult.

You’re probably asking yourself:

How much does a fintech app cost?

But here’s the question you should be asking:

What kind of fintech product are you actually building?

A personal finance tracker? A digital wallet? All of these have vastly different requirements.

And by vastly, we also mean different budgets.

The sooner you figure out the real cost drivers, the easier you can avoid expensive surprises later.

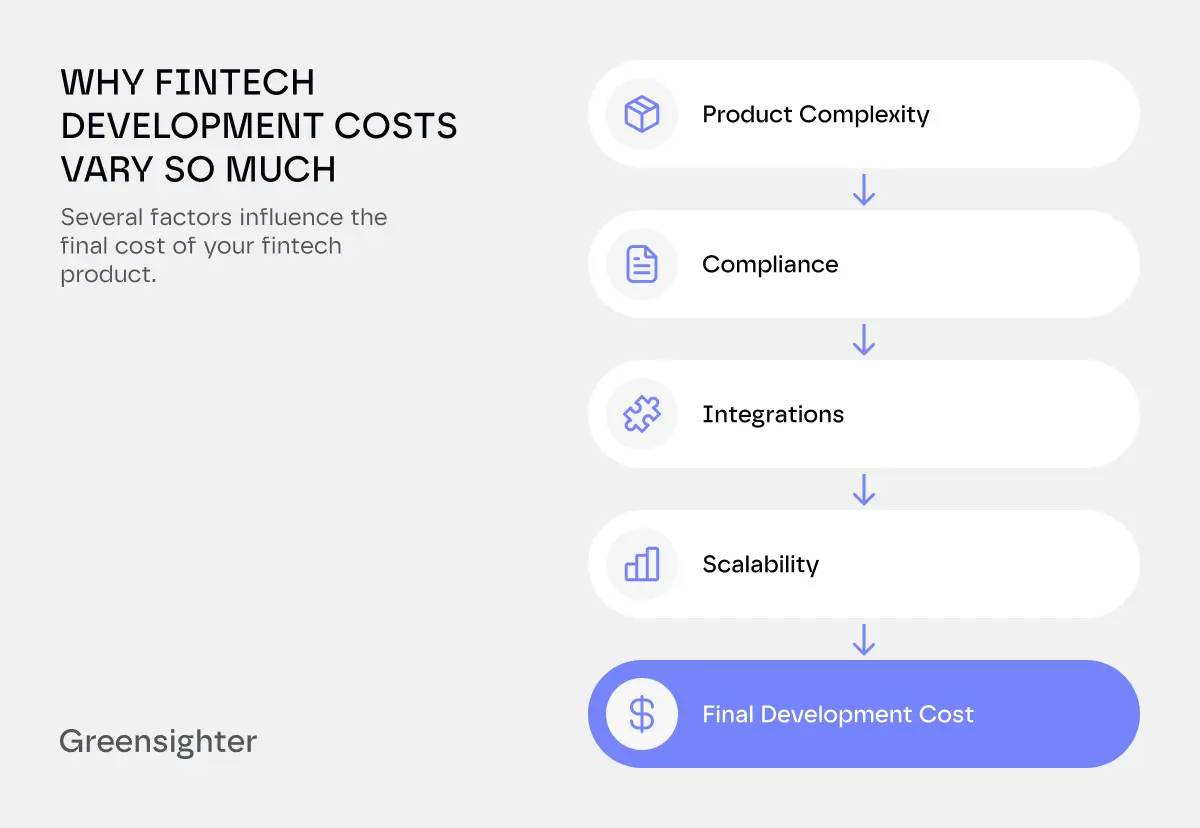

Why FinTech Development Costs Vary So Much

“All fintech products fall into the same category.” This is what most companies assume.

Nope, they don't.

A budgeting app costs far less to build than a regulated lending platform.

Likewise, a real-time payment solution has different requirements from an investment platform managing portfolios and market data.

The complexity behind the product determines the cost.

This is something we see across multiple industries.

Whether you're estimating a telemedicine platform, an EHR system, or a financial application, development costs depend:

- Scope

- Compliance requirements

- Integrations

- Long-term scalability planning.

Launch costs matter, but you also need to budget for what comes next.

And that’s where fintech projects often become cost-heavy.

The Biggest Factors Affecting FinTech App Development Cost

Several variables directly influence fintech app development cost.

Some are obvious.

Others stay under wraps until development is already underway.

Let's look at the biggest ones.

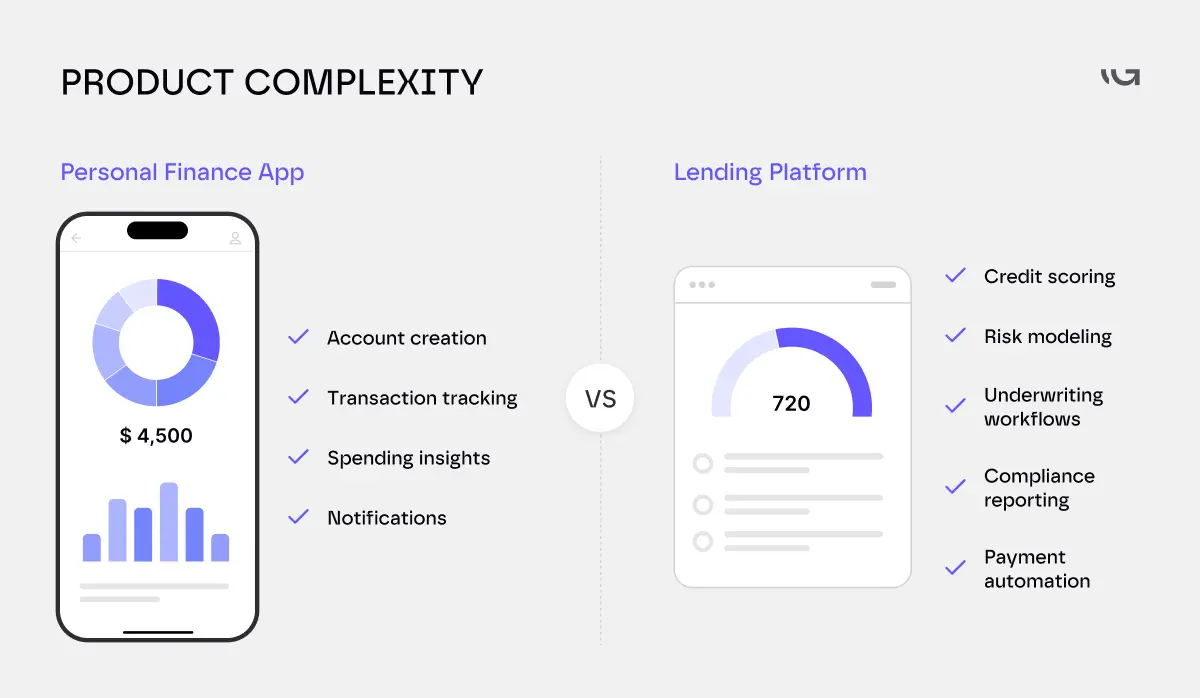

1. Product Complexity

This one’s a no-brainer:

The more sophisticated the product, the larger the budget.

A simple personal finance application may include:

- Account creation

- Transaction tracking

- Spending insights

- Notifications

A lending platform might come with:

- Credit scoring

- Risk modeling

- Underwriting workflows

- Compliance reporting

- Payment automation

Development effort and cost move in lockstep.

This’s why defining requirements early is critical.

Wondering why projects become expensive?

Likely because nobody clearly defined what success looked like before development began.

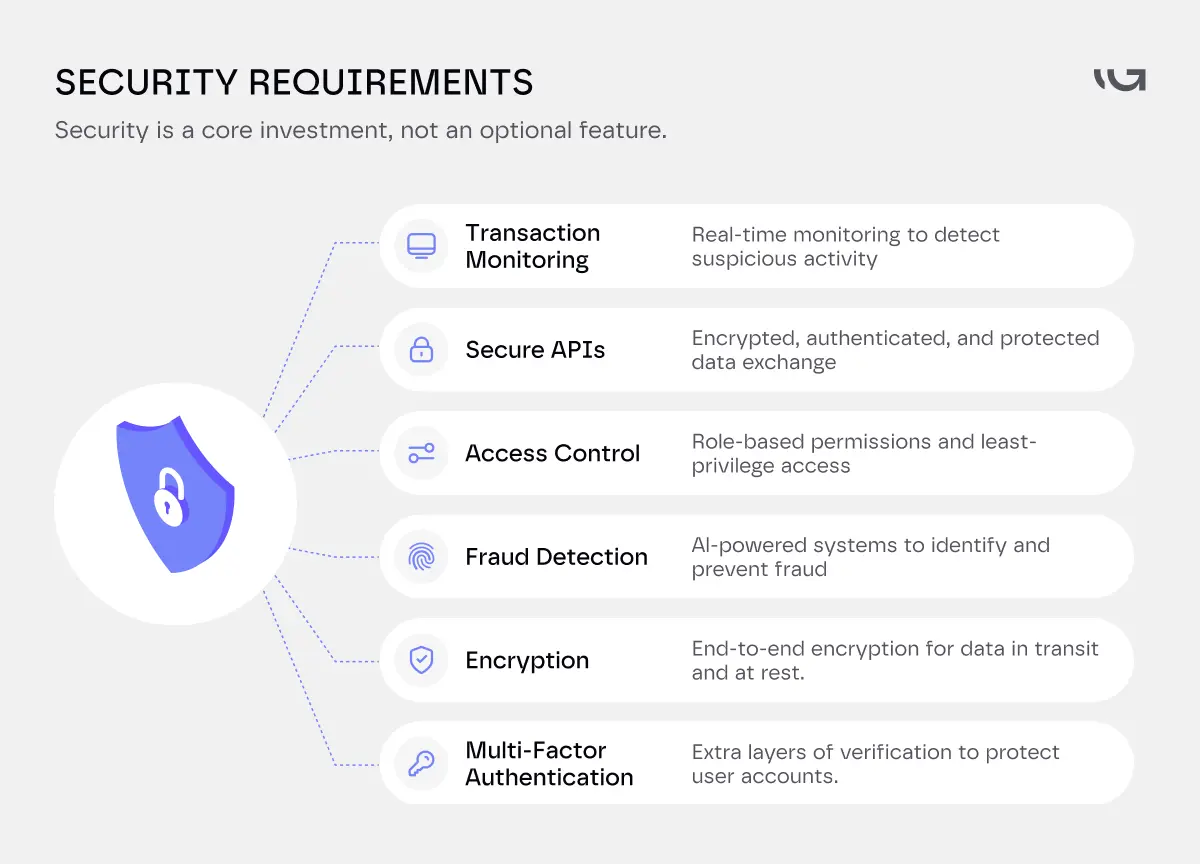

2. Security Requirements

Security is a large drain on resources in financial app development.

And it should be.

Financial products manage highly sensitive information.

Users trust these applications with:

- Personal data

- Banking information

- Payment credentials

- Financial history

This means you can’t treat security as a secondary consideration.

Common requirements include:

- Multi-factor authentication

- Encryption

- Fraud detection

- Access controls

- Secure APIs

- Transaction monitoring

These systems aren’t easy to implement, test, and maintain.

If the upfront cost feels high, that’s OK.

The expense of a breach is usually much, much higher.

3. Regulatory Requirements

Fintech products operate in one of the most regulated environments in technology.

Depending on the market and product category, organizations may need to address:

- KYC (Know Your Customer)

- AML (Anti-Money Laundering)

- PSD2 requirements

- Open Banking regulations

- regional financial regulations

This is what will happen if you underestimate the amount of work regulations introduce:

The product launches later.

The budget increases.

Or both.

Highly regulated industries often face similar development challenges.

Healthcare platforms, for example, encounter many of the same security, compliance, and infrastructure considerations.

Compliance should never be treated as something you solve at the end.

It influences architecture decisions from day one.

=cta=

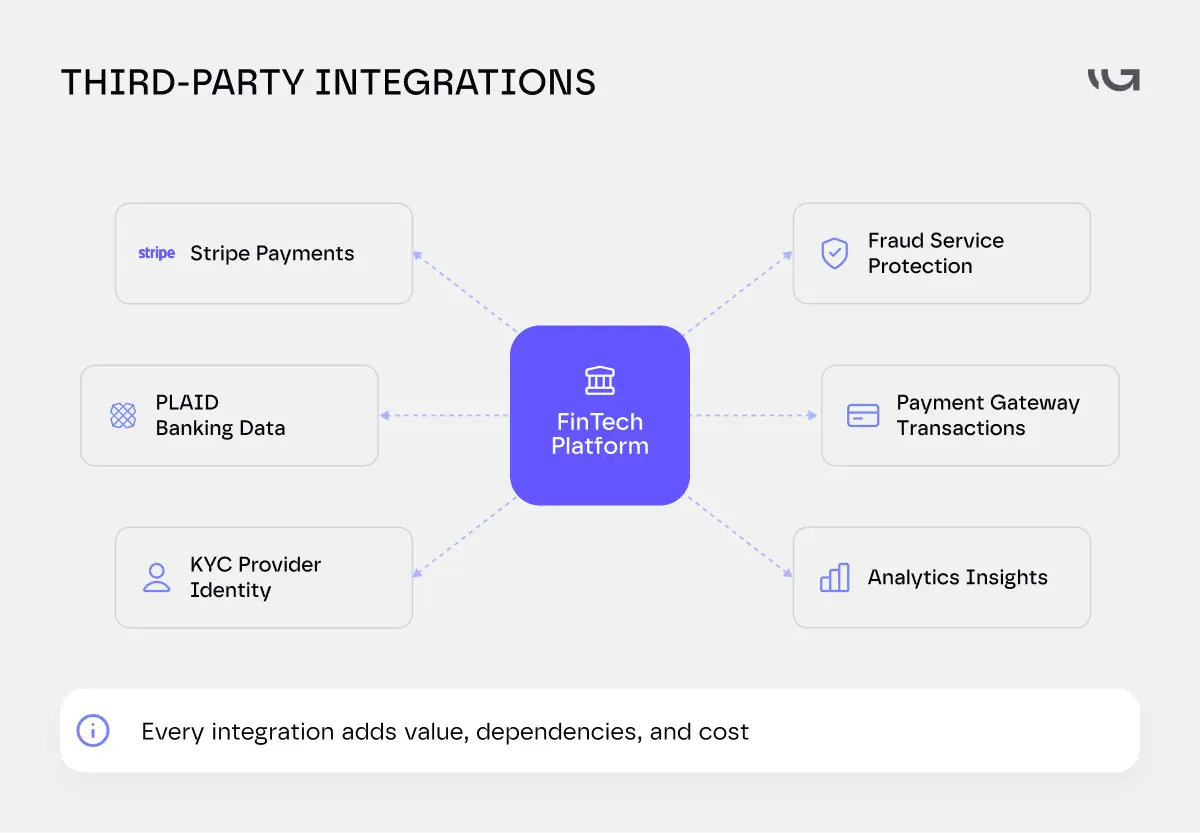

4. Third-Party Integrations

Modern fintech products rarely operate in isolation.

Most rely on external services for:

- Payments

- Banking connectivity

- Identity verification

- Fraud prevention

- Analytics

- Reporting

Examples include:

- Stripe

- Plaid

- banking APIs

- payment gateways

- KYC providers

WIth every integration, you require additional development effort.

That also comes with dependencies, and these in turn create risk.

A single integration can affect timelines, architecture, maintenance, and future scalability.

This is one reason why fintech app development often costs more than organizations initially expect.

5. Scalability Requirements

Many fintech products are designed around launch.

Few are designed around growth.

That creates problems.

A system supporting 1,000 users behaves very differently from a system supporting 1 million.

Scalability affects:

- Infrastructure

- Performance

- Database design

- Transaction processing

- Security architecture

You can reduce short-term expenses by ignoring scalability.

But this often increases long-term costs.

To design a strong fintech product, have growth in mind from the beginning.

6. Custom vs. Off-the-Shelf Development

At some point, you’ll end up at a familiar crossroad:

Build something custom.

Or assemble existing tools.

So, which path do you take?

There is no universal answer.

You can cut down on initial dev costs with off-the-shelf solutions.

But they often create limitations later.

Custom solutions are great, but they do require greater investment upfront.

The plus side? They offer greater flexibility, control, scalability, and differentiation.

This is where you might consider custom fintech software.

They work great for organizations with unique workflows, specialized products, or ambitious growth plans.

“What is cheaper?” shouldn’t be your go-to question.

Think of it this way: will the approach you take support the business five years from now?

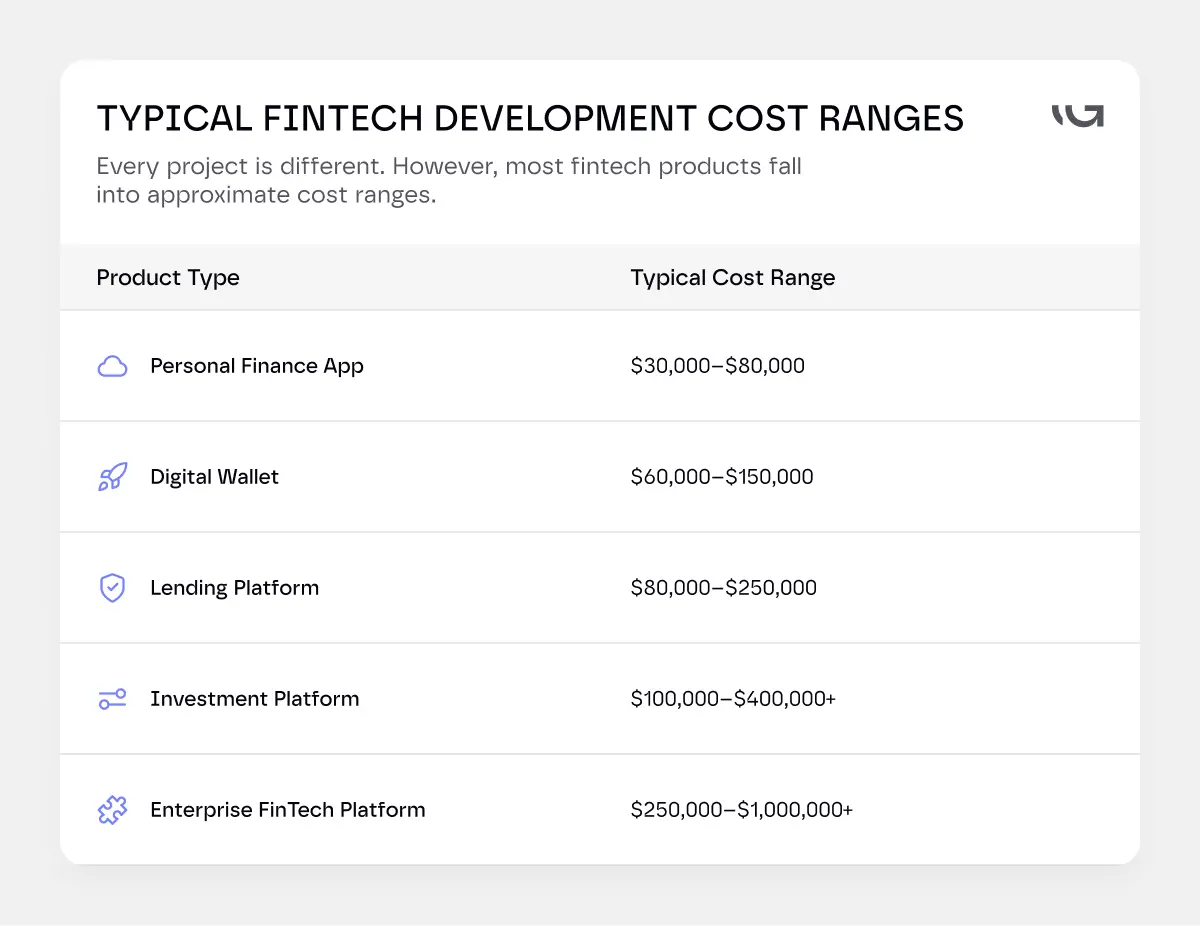

Typical FinTech Development Cost Ranges

Every project is different.

However, most fintech products fall into approximate cost ranges.

Product Type

They just show how pricing changes based on:

- Scope

- Compliance

- Integrations

- Security requirements

- Scalability expectations

Complexity and investment go hand-in-hand.

And in fintech, complexity gets there faster.

Hidden Costs Companies Forget to Budget For

Most discussions around fintech app development cost focus on visible features.

- The dashboard

- The payment flow

- The mobile experience

- The user interface

Those certainly affect pricing.

But they are rarely the reason projects go over budget.

The biggest surprises usually come from the operational requirements sitting behind the product.

These are the costs many teams fail to account for until development has kicked off.

Payment Infrastructure Is More Complex Than It Looks

A payment button is easy to imagine.

The systems behind it are a different story.

Modern fintech products often need to handle:

- Transaction reconciliation

- Payment failures

- Chargebacks

- Refunds

- Recurring payments

- Settlement workflows

These processes introduce significant complexity.

What looks like a simple transaction flow on the surface often requires extensive logic behind the scenes.

This is why development estimates are night and day between different financial products.

Reporting Requirements Grow Quickly

Most fintech products generate far more data than you expect.

Users want visibility into their financial activity.

Operations teams need performance metrics.

Compliance teams need audit trails.

Executives need business reporting.

As a result, many platforms end up building:

- Transaction histories

- Account statements

- Compliance reports

- Financial dashboards

- Operational analytics

These systems are rarely considered during early budget planning.

Yet they often become essential before launch.

Internal Teams Need Software Too

Don’t forget internal tooling when it comes to financial app development.

Your internal teams also use the platform.

And they need systems for:

- Customer support

- Account reviews

- Risk monitoring

- Fraud investigations

- Transaction disputes

Without proper administrative tools, operational efficiency suffers.

That’s why we recommend investing into back-office systems alongside customer-facing features.

The customer application may be the product everyone sees.

The operational platform is often what keeps the business running.

Legacy Systems Create Unexpected Costs

Not every fintech product starts from scratch.

You may need to integrate with existing infrastructure.

This can include:

- Legacy databases

- Banking platforms

- Accounting systems

- Payment processors

- Customer records

These integrations are often far more complex than anticipated.

Data inconsistencies.

Migration challenges.

Compatibility issues.

Operational dependencies.

All of these can increase timelines and development costs significantly.

The Real Budget Killer Is Complexity

One major feature won’t make your fintech projects expensive.

That will happen once complexity piles up.

A new integration here, additional reporting there.

Extra compliance requirements.

Unexpected operational needs.

These seem manageable on their own.

Put them together, however, and a modest project transforms into a major investment.

Common Budgeting Mistakes

Your fintech project isn’t failing because of technology.

It’s failing because of assumptions.

Let's look at some of the most common mistakes that inflate fintech app development cost.

Underestimating Compliance

That tricky thing about compliance is that it often looks manageable on paper.

Then you start implementation.

- Identity verification

- Record keeping

- Reporting requirements

- Audit readiness

The reality is usually more complicated than expected.

And more expensive.

That’s because compliance is an operational layer that influences the entire product.

Assuming Integrations Are Simple

Nothing is simply plug-and-play when it comes to integrations.

Every external service has baggage:

- Technical dependencies

- Testing requirements

- Maintenance obligations

- Operational risks

The integration itself is often the easy part.

Managing it over time is where things get tricky and expensive.

Treating Security as a Later Phase

If you’re launching fast and improving security later, stop.

This usually creates technical debt.

Security architecture becomes harder and more expensive to implement after building core systems.

In fintech, delaying security decisions is rarely a cost-saving strategy.

The opposite, actually. It’s a cost-multiplying strategy you don’t want.

Planning for Launch But Not Growth

You’ve probably budgeted for version one.

What about version ten? Because there will be a version ten.

Growth introduces new challenges:

- Infrastructure expansion

- Performance optimization

- Additional compliance requirements

- Larger support teams

- Increased security demands

Products designed only for launch often require expensive restructuring later.

Final Thoughts

There is no universal answer to fintech app development cost. We wish there was.

Every product has different requirements.

Different risks.

Different compliance obligations.

Different growth expectations.

What matters is understanding where the real costs come from.

Security, compliance, integrations, scalability, operational complexity.

These factors influence budget far more than design screens or feature lists.

The companies that plan for them early tend to keep unexpected costs under control.

FAQs

How much does fintech app development cost?

It changes depending on complexity, security requirements, compliance obligations, integrations, and scalability needs.

Simple fintech products may cost tens of thousands of dollars.

Enterprise platforms can exceed several hundred thousand dollars.

What affects fintech app development cost the most?

The biggest cost drivers usually include:

- Product complexity

- Compliance requirements

- Security architecture

- Third-party integrations

- Scalability planning

These factors often have a larger impact on budget than visual design.

Is custom fintech software worth the investment?

For many businesses, yes.

Custom solutions offer greater flexibility, scalability, and control over product development.

While the initial investment may be higher, they often reduce long-term operational limitations.

How long does fintech app development take?

Timelines vary depending on scope.

A simple product may take several months.

More sophisticated financial platforms can require a year or more of development and testing.

What features increase financial app development costs?

Security systems, payment processing, compliance workflows, reporting tools, fraud prevention, and large-scale integrations are often among the most expensive features.

How can companies reduce fintech app development cost?

The best approach is proper planning.

Clear requirements, realistic scope definition, early compliance planning, and scalable architecture decisions help prevent expensive changes later.